Featured Post: My Reading & Podcast List

Here are recent books I’ve read and podcasts I enjoy. If you’re looking for something interesting to listen to or read, these are a few that have stood out to me. Let me know if you have a recommendations.

2017 Email Marketing Report Card: Did Your Program Make the Grade?

As 2017 finds itself in your rearview mirror, ask yourself a question. What changes did I make to my email program in 2017 that had a significant impact? It’s a simple question, but I bet many of you won’t have a good answer. Some of you are likely doing the same thing now at the end of the year that you were at the start of it, possibly due to the rush of day-to-day execution or limited internal resources.

Here’s a checklist to help you plan for 2018:

As 2017 finds itself in your rearview mirror, ask yourself a question. What changes did I make to my email program in 2017 that had a significant impact? It’s a simple question, but I bet many of you won’t have a good answer. Some of you are likely doing the same thing now at the end of the year that you were at the start of it, possibly due to the rush of day-to-day execution or limited internal resources.

But email continues to be a powerful marketing tool. According to Econsultancy, 73% of in-house marketers worldwide said that email marketing provided a strong ROI, the most of any marketing channel. Yet, it’s too often overlooked or taken for granted.

While you may be planning to grow your email ROI in 2018, it will require some reflection and careful planning. Take a good hard look at where your program started and ended the year, and why you did or did not accomplish your goals.

Here’s a checklist to help you plan for 2018:

Review your previous goals. What were your 2017 email marketing initiatives? If you didn’t commit to any specific goals in 2017, keep reading. Now’s the time to start planning and setting goals for the coming year.

Document major accomplishments. Look at your program from the top down. What were your major accomplishments from this past year? Did you implement any new email programs, such as browse recovery? If so, how are they performing?

Optimize your messages. If you made an effort to optimize your messaging in 2017, how has it performed? Did the changes work as intended? If not, why? If so, how can you apply these principles to other messages in 2018? Don’t stop there. How can you further optimize your messages in 2018?

Assess incomplete goals. Which initiatives are left undone, and why? What roadblocks prevented you from accomplishing your goals, and how will you overcome them in 2018? And here’s another question. How much revenue did you leave on the table by not reaching these goals?

Plan for 2018. What key initiatives do you want to achieve in 2018? How much will each help your overall email program?

Analyze your resources. If you realize that you simply can’t get things done, ask for help. Find someone internally who can lend a hand. Look for partners, such as your email provider, who might be able to guide and assist you with executing your vision. Find outside third parties who may be able to help. There’s no shortage of help out here.

Don’t set it and forget it. Always look at the numbers and identify areas for improvement. If you don’t change the oil in your car, it will eventually stop working. The same goes for your automated messages. Consider editing subject lines, freshening up hero images, changing verbiage, updating template layouts, and split-testing multiple versions of your messages. What looked good two years ago may be stale and out of date today.

Don’t stop with best practices. Just because you implemented new programs this year doesn’t mean they can’t be improved. Remember: Best practices are not the endpoint, but rather the starting point. How can you make these messages more relevant for your subscribers?

Doing the same thing and hoping for better results is not only impractical, but it’s not a sustainable model for success, particularly now that consumers are more in control and expect more from retailers. If you haven’t done so yet, it’s time to come up with your roadmap for improvement. Perhaps you’ll focus on product recommendations, behavioral segmentation, optimized automated messages, user-generated content, or a combination of them all. I recently wrote about several strategies for doing just that.

With so much available out there to help you improve your email ROI, you should be asking yourself not “What can we do?” but “How much can we do?”

This was originally published on Multichannel Merchant.

Why Amazon is trying to out‑Walmart Walmart

Cash is king. Well, actually, Amazon is king. And it certainly creates a lot of cash. Not only does Amazon continue to dominate e-commerce, but it also impacts almost every line of business—from supermarkets to web services. Now it’s even getting into pharmaceuticals.

The folks over at Amazon are not dumb. They test, and they try. Often times, they even fail. But while they push the limits of getting to market, they’ve also proven to be patient. More importantly, they’re very calculated.

Cash is king. Well, actually, Amazon is king. And it certainly creates a lot of cash. Not only does Amazon continue to dominate e-commerce, but it also impacts almost every line of business—from supermarkets to web services. Now it’s even getting into pharmaceuticals.

The folks over at Amazon are not dumb. They test, and they try. Oftentimes, they even fail. But while they push the limits of getting to market, they’ve also proven to be patient. More importantly, they’re very calculated.

Walmart is trying to become Amazon. Ironically, though, I see Amazon as actually trying to become Walmart. Why? Because while e-commerce is growing, 92% of retail sales come from brick-and-mortar stores. Brick-and-mortar sales will continue to give up share to e-commerce, but e-commerce won’t replace it. People will continue to shop in-store, and Amazon knows that.

Here’s why I think it makes sense for Amazon to get into the supercenter game. I’m sure they’ll come up with a snazzier name, but let’s call it Amazon Life. Anyway, let’s explore this a bit, shall we?

Brick-and-Mortar: We all know Amazon is no longer an ecommerce pure-play. It has its own book stores, it now has Whole Foods (and is expanding pick-up lockers in some locations), it has stand-alone pickup lockers, and it’s also partnered with Kohl’s. This partnership makes Kohl’s a return hub for Amazon customers, as well as a place to purchase some Amazon products, such as the Echo. From what I can tell, the only reason Kohl’s agreed to this is that they believe in the “if you can’t beat ‘em, join ‘em” philosophy. I don’t see this ending well for them.

I envision Amazon using Kohl’s as a testing ground to track how many returns are actually made at these locations. Are people willing to drive to a physical store to make returns? If so, how frequently? Will this additional flexibility increase the rate of return, or will it remain steady? I’ll bet Amazon is analyzing this very closely.

Kohl’s, on the other hand, is likely banking on the idea that when someone returns an item, notably clothing, they might stick around to shop for better-fitting replacement items. While this makes sense, it’s not sustainable. Amazon offers too many products for Kohl’s to bank on generating enough clothing returns and related sales to expand its market share. Amazon has over a dozen private labels in the clothing category alone and is showing no sign of slowing its expansion in this category. Why would Amazon want to potentially lose sales to Kohl’s, whose shoppers are the perfect demographic for some of its own product lines?

Shipping costs continue to rise and eat away at margins. Having a more central location where consumers could pick up orders, even same day, could cut these costs significantly. According to fulfillment software vendor Temando, 82% of shoppers said they want the option to buy online and pick up in-store. The cost of paying for returns would be significantly reduced as well. Much like the Kohl’s model, consumers would bring their returns to the store. And, oh yeah, as with the Kohl’s theory, people may want to shop for a new size or product to replace the return while they’re there. The good news here is that all the money would stay with Amazon.

Amazon’s private labels. They continue to be big sellers, and they’re constantly expanding. This includes the most recent launch of Amazon’s first two furniture lines. With over 30 private labels, there will be no shortage of products to display in-store, especially with the fashion lines. I’m going to guess that clothing makes up a large percentage of Amazon’s returns. And with the investment made in the Amazon Look [the version of Echo with a built-in camera], having a local store to assemble a wardrobe for try-on makes sense. It should also help reduce back-and-forth shipping costs under the current Prime Wardrobe subscription model.

The Whole Foods play. The chain is already a brick-and-mortar presence with over 400 stores, but they’re often cramped. Being able to buy groceries (even for pickup) while grabbing a new USB charger, a pair of socks, and your prescription refill all in one stop certainly sounds like a win-win for consumers. It has been for Walmart. This combination into a supercenter format should allow for a more streamlined distribution process.

Amazon pharmacies. While it doesn’t yet have the permits to operate an actual pharmacy, Amazon is certainly going to get there. Now, unless it purchases a drugstore chain (which is quite possible), it will have to either build out stand-alone drug stores (too costly), integrate them into an already cramped Whole Foods space (not likely), or simply be mail-order-only (least likely).

Amazon warehousing and fulfillment. Consolidation into storefronts could provide Amazon with even more leverage when dealing with brands to use its warehouse and fulfillment services. Knowing consumers could buy and pick up same-day would create some urgency for brands to want to keep their product both in stock in stores and for quick shipping online. Brands would likely need to pay for larger Amazon warehousing, increasing Amazon billings.

Showrooming. Of course, consumers love showrooming. Just ask Best Buy! This is especially true for larger purchases, such as TVs. Too bad Amazon doesn’t sell electronics. Oh, wait. You won’t need to visit a showroom and then check Amazon for its price.

Data suggests that millennials and Gen Zers actually like going into stores, but they’re also quite comfortable shopping online. More importantly, they value time, convenience, and the experience. Many retailers lack a focus on the in-store customer experience. Amazon doesn’t—and won’t. You can bet that people walking into an Amazon Life (name not official) location would be greeted with convenience and excellent customer service.

Could This Change Prime Memberships?

Consider this. If all of this happened, Amazon might have the ability to differentiate Prime offerings, such as Prime Standard and Prime+. How would they differ?

Just hypothesizing, Prime Standard could be similar to what you have today. Free two-day shipping and free returns, as well as other media-type services. There would remain a charge for Prime Pantry deliveries; however, instead of offering same-day delivery for free, you would instead have access to same-day pickup at one of their locations.

Prime+ could be offered at a slightly higher price point and include the same-day delivery as an added option. You may even have the delivery charge for grocery orders waived one time each month. You could look for other added benefits to either program, such as tying in meal or fashion subscription services in some way.

So, while Walmart is chasing Amazon, I think Amazon quietly has its sights set on being more like Walmart. Being able to physically provide a customer-centric experience that Prime and non-Prime members alike have come to expect from Amazon can go a long way toward further cementing customer loyalty to the brand.

Brick-and-mortar isn’t dead. It just needs to be done better! And I bet Amazon will be just the one to prove it to us.

This was originally published by Internet Retailer.

New Year, New Emails, No More Excuses

With email continuing to be one of the top-performing online marketing channels, I guess it shouldn’t be a surprise that my inbox is overrun with bland, generic emails. Why change what seems to be working? But change is inevitable. If you don’t believe me, just look at what evolving consumer expectations have done to many legacy retailers.

The fact is, while some strategies require larger resources or investments, many do not – and those that don’t can pay huge dividends. Make 2018 excuse-free. Roll up your sleeves, and improve your email program. Here are three ways to get started.

With email continuing to be one of the top-performing online marketing channels, I guess it shouldn’t be a surprise that my inbox is overrun with bland, generic emails. Why change what seems to be working? But change is inevitable. If you don’t believe me, just look at what evolving consumer expectations have done to many legacy retailers.

First, a look at some numbers. The Relevancy Group reports that U.S. marketing executives attribute 23% of total revenue in Q2 2017 to email, a 21% year-over-year increase. But other research suggests consumers expect more. A Flagship Research report from 2016 showed that 62% of consumers expect website browsing behavior to be used to personalize emails, and 76% expect the same with purchase history. Relevance matters to consumers, especially when it comes to marketing emails.

Traditional promotional emails can still deliver revenue, but relevant, personalized emails can deliver much more. I know, you don’t have a lot of resources at your disposal. I know, it’s only you running the show. And yes, I know you already have a welcome series (well, really, I hope you do). But I also know an excuse when I hear one.

The fact is, while some strategies require larger resources or investments, many do not – and those that don’t can pay huge dividends. Make 2018 excuse-free. Roll up your sleeves and improve your email program. Here are three ways to get started.

Step 1: Reassess Your Welcome Series

If a 60-year-old man and an 18-year-old woman sign up to receive your emails, will they receive the same welcome series? If the answer is yes, you need to make adjustments. Consumers expect relevance. Sending the same message to both subscribers is not that.

There are a couple of ways to do this. Look at what page, or category, the sign-up came from, and deliver specific messaging based on the acquisition source. If they signed up from the maternity category, customize their messaging to match. If they signed up on the men’s swim trunks page, do the same. Apply this strategy not only to the first message, but the entire series as well. Tracking the source is easy to do with a simple piece of source code, a field identifier or by using a unique sign-up form. The best part is that you can implement this tracking before any messages are even created, which gives you valuable segmentation information on your subscribers before new welcome messages start sending.

In lieu of this tactic, or in addition to it, determine the welcome series based on the actual clicks inside of your welcome email. If a subscriber receives a generic welcome message and clicks on the maternity navigation bar link, the next message should be maternity-focused. The same goes for other clicks. This allows subscribers to control their own onboarding experience. One company that tried this saw increases in every email metric for the customized message versus the generic one. The personalized message generated 140% more revenue than the generic version, while making up only 3% of the volume of sends.

In both instances, setting up the automation and tracking the data are extremely easy to do. And messages can be created and implemented one at a time. Gradually implementing new messages will require fewer resources for execution because it’s not an all-at-once strategy. As a bonus, think about all of the segmentation data you’ll capture with this click behavior while implementing your plan.

Step 2: Personalize Your Cart Recovery Strategy

Should a customer abandoning $800 worth of products receive the same message as the customer who abandoned one $50 item? Their obstacles to conversion and motivations for purchase are likely very different. Yet, in most cases, each gets the same message.

Why not customize the message to overcome potential hurdles? You have a lot of cart data readily available that can help you make these messages more relevant. For products themselves, look at things like cart total, SKUs, product category, margin of products, sale price, what gender would likely use it and/or sale end date. Consider the actual shopper by looking at their purchase history, such as recency of last purchase, lifetime AOV or total number of orders.

Such data can help you determine how to overcome conversion obstacles and what types of messages to communicate to the would-be buyer, including when to send them, how many to send, and what types of incentives to offer, if any. Addressing the shoppers’ needs – for example, communicating about installation and haul-away services for specific cart SKUs – can be a great way to address the individual shopper. Personalizing messages in a meaningful way, while protecting margins, lets both customers and retailers win.

Step 3: Think About What They Want

While relevant lifecycle messages can drive significant revenue, so too can your promotional messages. Crafting 50 segments to use in daily promotional emails isn’t realistic for most retailers, but you don’t have to settle for generic batch-and-blast messaging either. Inserting intuitive product recommendations into your emails is an excellent way to make emails more relevant.

Using product recommendations that take into account individual browsing and purchase history, email content, and even your select business rules can deliver powerful results. Think about your everyday promotional email sends. With a batch-and-blast strategy, each message is relevant to only a portion of the audience at any one time. With individual recommendations, some part of that message will be relevant at all times.

Include recommendations not only in your promotional messages but also in any triggered message, such as order and shipping confirmations, birthday messages, post-purchase messages, and even cart abandonment emails. You can even use recommendations as stand-alone email content. In addition to being relevant, these types of emails provide a nice change of pace from the standard promotional messages.

The best thing about using product recommendations is that they don’t require extra resources, so you can still focus on growing your email ROI. How does generating 33% more revenue from your emails sound? That’s what one company saw from emails sent with recommendations versus those without. People like personalization.

“Get Busy Living or Get Busy Dying”

This line is from one of my favorite movies, and it sums up email marketing perfectly. Being complacent with your email program in 2018 is not the key to success. In fact, it may be the ticket to gradual failure. With competition coming from every direction, consumers are quick to tune it out. Personalization can help you cut through the noise. Are your emails differentiating you from your competitors? Do they give consumers what they want? If not, 2018 is a perfect time to ditch the monotonous one-size-fits-all messaging and get personal.

This was originally published on Multichannel Merchant.

Eggnog and Fruitcake: Holiday Predictions That You Can Stomach

With the holiday shopping season about to begin, I thought this would be the perfect time to share my expectations for the end of the year. After all, planning is all about anticipation, and knowing what to anticipate will help you better prepare for the holidays. Here goes:

With the holiday shopping season about to begin, I thought this would be the perfect time to share my expectations for the end of the year. After all, planning is all about anticipation, and knowing what to anticipate will help you better prepare for the holidays. Here goes:

More Billion Dollar Days. 2016 saw 57 of 61 days in November and December rake in $1 billion in online sales. This year, I expect to see 60 of 61 days hit that mark. Why not all 61? Everyone needs a day to rest.

More Mobile Sales. Last year, mobile commerce grew nearly 54% during the holidays and accounted for 30% of all online sales. Mobile sales have been increasing year over year, and this trend will continue. Be sure you’re optimized for mobile because I expect it will account for roughly 35% of all online holiday sales.

And Even More Mobile Clicks. In Q4 2016, mobile accounted for nearly 57% of paid search clicks, with 47% coming from smartphones. Expect this to continue. Mobile is no longer a trend; it’s the way most consumers shop – at least some of the time. The smartphone is now the primary device that the majority of internet visitors use to access the internet. And in the not-so-distant future, it’ll be their primary device for buying online.

Promotions and In-Store Sales

Early Sales. Online holiday sales will start in October. Retailers have been discounting earlier and earlier to get a jump-start on their competition, turning Cyber Weekend into a month-long event that I like to call Gray November. But with Amazon taking in nearly 40% of all online sales last holiday season, and Prime memberships continuing to rise, retailers have even more to lose by not getting an early start.

Exclusions Apply. For the past several years, especially last year, I saw a noticeable trend in holiday sales having mass exclusions. As a heavy shopper during this period of time, I found myself frustrated. But frustrated or not, I expect this trend to continue. You will see fewer “off everything” promotions and an increase in discounts on “select items.” If you plan to restrict sales, be clear as to what is – and isn’t – included.

In-Store Exclusives. You may see a rise in brick-and-mortar retailers offering “off everything” or deeper discount sales for in-store only. This allows a retailer to drive that sought-after in-store traffic, while offering shoppers deeper discounts and no shipping fees. Seems like an obvious win-win.

Re-engineering the Brick-and-Mortar Experience. I expect in-store sales to increase from last year, but not as much as ecommerce sales. You’ll see a large push from multichannel merchants to drive in-store traffic, touting extra incentives for shopping in-store and even discounts for in-store pickup. As 65% of consumers make additional purchases when going in to pick up items, the tactic makes a lot of sense. Expect to see in-store-only Black Friday and Cyber Monday sales (likely all weekend long), as well as some in-store price-matching. While never a long-term model for success, many retailers may find it worthwhile during the holidays.

The Big Shopping Days

Black Friday and Cyber Monday. While no longer the start of the shopping season, these days are still known as deep discount days. Shoppers oblige and spend more online on these two marquee days than any others during the year. But which day is bigger?

Both days will drive over $1 billion in mobile commerce.

For the first time, Black Friday –not Cyber Monday – will be the largest online shopping day of the year.

Of course, the marketing and promotions for these days will start on the Sunday or Monday prior.

Thanksgiving Day. This will continue its growth as an online shopping day and cross $2 billion in online sales for the first time ever.

Marketing Tools, Top Gifts and the Obligatory Amazon Mention

Browserless Commerce. Speaking of the Echo, voice assistants will be the hottest sellers of the season. While I predict Amazon devices to be the number-one sellers in this group, Google and Apple will see significant sales in this arena. The age of voice is upon us. “Hey Santa, bring me a new train set.”

Email Marketing. Email will continue to dominate as an online marketing tool during the holidays. Last year, Bronto sent 50% more messages than they did during Black Friday and Cyber Monday 2015, sending more messages in November than ever before in company history. I know my inbox will be busy.

Amazon’s Take. Amazon captured 38% of the online holiday sales last year, and it will once again own a substantial portion of the holiday ecommerce space. With the rise in Prime memberships and adoption of the Echo, I would not be surprised to see this figure inch up to the 45% mark.

Three Even Bolder Predictions:

Starbucks will take flack over its holiday cup design. ‘Tis the season!

I will once again purchase my tree on Black Friday.

Fruitcake, while good in theory, will continue to be a poor party dessert.

What could go wrong? Apart from the hostility of rogue nation states, what else could throw holiday shopping into a tailspin? How about fallout from the Equifax data breach? Potential widespread credit card fraud resulting from this breach could put a major wrench in holiday spending and shopping habits. Credit cards could be frozen due to fraud, consumers could lose trust in online security when purchasing, and it could over-inflate online sales data if fraudulent sales are racked up. There have already been reports of a 15% increase in fraud as early as August of this year. This lack of trust in security might wind up benefiting major, name-brand retailers, as many consumers tend to put more trust in them.

What do you think you’ll see this holiday season? I plan to watch my inbox, shop my exclusionary sales online, and sip my coffee from a ridiculed Starbuck’s cup, all from the comfort of my living room. Just don’t be a Scrooge and charge me for shipping!

This was originally published on Multichannel Merchant.

Key Holiday Trends That Keep on Giving

Commerce marketers seem to start preparing for the holiday season earlier and earlier each year – and with good reason. Consumers now start their holiday shopping earlier than ever. Getting ready for such an early shopping season can come with great challenges, but there’s no need to reinvent the wheel. Take a look at the trends over the past couple of years, especially those from last year, and identify opportunities for success. Here are two of the trends I noticed last year that can help you set the stage for a successful season.

Commerce marketers seem to start preparing for the holiday season earlier and earlier each year – and with good reason. Consumers now start their holiday shopping earlier than ever. Getting ready for such an early shopping season can come with great challenges, but there’s no need to reinvent the wheel. Take a look at the trends over the past couple of years, especially those from last year, and identify opportunities for success. Here are two of the trends I noticed last year that can help you set the stage for a successful season.

Trend 1: Self-Gifting and Discounting

While people are shopping earlier in the season, it’s not necessarily for others. The trend of self-gifting has been increasing over the years for a variety of reasons, including early access to discounts, social influence, the economy, and constant consumer connectivity.

In 2016, 57 of 61 days in November and December generated $1 billion in online sales, including 29 of 30 days in November. To put this into perspective, Cyber Monday 2010 was the only billion-dollar day that season.

Retailers who want to secure sales before their competitors have been offering deeper discounts earlier in the season, which has turned what was once a month leading up to the ever-popular Black Friday and Cyber Monday into Gray November, a month-long discounting period. Now, those two days, while still prominent, are merely a part of it.

Takeaways:

Start your marketing early! Waiting until Black Friday rolls around means you’ll be losing out on sales and leaving money on the table. Consumers will shop early, so plan to start your holiday push in late October or very early November. But just because you start marketing early doesn’t mean you need to run your deepest promotions from the get-go.

If you plan on discounting, start by offering sales and promotions that can help protect margins. Test promotions such as tiered discounts, where you earn a deeper discount by hitting certain spend thresholds. Consider offering free gifts, flash sales, or special sales on specific categories or groups of products. They can all encourage shoppers to buy for themselves and for others while doing more to protect your overall margins.

Trend 2: Black Friday, Cyber Monday and Other Key Dates

As I said, Gray November has dethroned Black Friday as the start of the shopping season, but that doesn’t mean Black Friday and Cyber Monday are dead. While they’re no longer the standalone days of yesteryear, they’re still popular with shoppers and remain marquee shopping days. Last year, they were the two biggest online shopping days in history, with Cyber Monday leading the way.

According to Adobe Digital Insights, Black Friday generated $3.34 billion in online sales (and was the first day ever to do $1 billion in mobile commerce), while Cyber Monday saw $3.45 billion in online sales. Interestingly, Black Friday saw a 21% increase in online sales from the year before versus just 12% for Cyber Monday. From an online sales perspective, Black Friday is growing faster than Cyber Monday. If this trend continues, expect Black Friday 2017 to become the biggest online shopping day in history.

Online retailers have a tendency to focus on Cyber Monday, but doing so is a mistake. If you wait until Cyber Monday to run your peak deals, you may miss the chance to capture sales. Come December, the shopping season is only getting started. Remember, 57 of 61 days in the last two months of the year had over $1 billion in online sales. Once the calendar flips to December, don’t let up. If customers are self-gifting, they still have lots of room to buy for others.

But December also brings procrastinating shoppers and shipping deadlines. You must create a sense of urgency when deadlines are approaching. The last thing you want is for consumers to run off and sign up for Amazon Prime to get quick, free shipping because they waited too long.

Brick-and-mortar retailers have been making a conscious effort to drive buy online, pick up in-store purchases. After all, it’s a win-win approach. It satisfies the consumer’s need for immediacy, and 65% of customers make additional purchases when picking up orders in the store. If you offer this service, be sure to advertise it all season long.

Takeaways:

When planning your best deals, consider not only the impact of Gray November but also how Black Friday and Cyber Monday are treated. Start early by marketing the week leading up to these days as Cyber Week. Many retailers already do this to get a jump on their sales while still taking advantage of named days, such as Black Friday. Considering Amazon accounted for 38% of all holiday sales last year, it’s critical to maximize revenue this holiday season.

If you have brick-and-mortar locations, focus on buy online, pick up in-store callouts. With UPS’s surcharge on holiday shipping, this may be even more important this year. If you can, use geolocation to identify the nearest store for the consumer inside your email or on the website itself. This tactic will be especially critical once shipping deadlines have passed. To encourage the use of this tactic, consider offering a free gift, such as stocking stuffers, for orders picked up in the store.

When it comes to email marketing, subject lines can tell a lot. Looking at my own inbox during the 2016 holiday season, three interesting things stood out to me:

On Thanksgiving Day, 34% of emails I received used the term “Black Friday” – only 20% used “Thanksgiving.”

On Sunday, November 27, “Cyber Monday” was used in 21.8% of emails, while “Black Friday” was still being used in 14.4%.

In late December, only 12 emails out of thousands included my first name. It’s much more important to focus on the value you’re offering in these messages than the recipient’s name.

There’s no magic formula for success when it comes to planning for the holiday season. But preparation is key. Look at consumer and retail trends, as well as your own historical data, to help determine what will be successful this season. Whether it’s online or in-store, consumers will find deals that suit them, and they’ll start shopping early. They just no longer need to throw elbows to get those deals, although someone probably will.

This was originally published on www.bronto.com

3 Holiday Trends: Prepare for the Marathon, Not a Sprint

The holiday shopping season is the ecommerce version of the Boston Marathon’s Heartbreak Hill. It’s a season that will challenge retailers, stress them, push them to their limits and, many times, either make or break them. Effectively planning for the final stretch requires not only looking at last year’s results, but considering what went well for your peers. Let’s look at three trends from last year that will keep you from hitting the wall this year.

The holiday shopping season is the ecommerce version of the Boston Marathon’s Heartbreak Hill. It’s a season that will challenge retailers, stress them, push them to their limits and, many times, either make or break them. Effectively planning for the final stretch requires not only looking at last year’s results, but considering what went well for your peers. Let’s look at three trends from last year that will keep you from hitting the wall this year.

Every Day Is a Holiday

Last year, 57 of the 61 days in November and December generated over $1 billion in online sales. In November, 29 of 30 days reached this major milestone. The rise of consumer self-gifting and the tendency of retailers to offer earlier and deeper discounts have contributed to this trend. Premier stand-alone days like Black Friday and Cyber Monday have increasingly given way to Gray November, a month-long discounting period, and consumers have quickly bought into it.

When preparing for the holiday season, don’t wait until Black Friday week. Treat the season as a marathon, not a sprint. Many of your competitors will begin their holiday marketing when the calendar flips to November, if not sooner. Planning for an extended holiday season will allow you to better balance the types of promotions and discounts you offer.

Mobile Is King

We all know mobile shopping is growing, and last holiday season really proved that. Mobile accounted for 30% of all online holiday sales, growing nearly 54% and outpacing that of not only retail (4.8%), but also ecommerce (17.8%). Mobile purchasing is becoming more prevalent each year. Expect this trend to continue.

If people are searching more via mobile devices, you would expect paid ad results to follow a similar trend. Predictably, they did. The percentage of paid search clicks on mobile devices has been steadily rising year over year. In Q4, it accounted for nearly 57% of all paid search clicks, with 47% coming from mobile phones. In 2015, those numbers were 48% and 32.6% respectively. When planning your paid search spend this holiday season, factor in which devices you are targeting with that budget.

The Resurgence of Black Friday … Online

Everyone knows Black Friday and Cyber Monday have historically been premier seasonal shopping days. But with the emergence of Gray November, they are no longer the “start” of the shopping season – they’re merely a part of it. In some respects, they even mark the final days before gift-giving and stocking stuffers become the major marketing theme.

As we know that promotions and consumer shopping now starts at the beginning of November, it’s important to plan your special sales around these key dates. Let’s look at what we’re seeing play out between these two premier days.

Last year, Black Friday online sales totaled $3.34 billion. At that time, it was the largest online shopping day in history. Not only that, but this was the first day ever to see $1 billion in mobile commerce.

The title of history’s largest online sales day lasted only a couple of days, however, as Cyber Monday edged it out with $3.45 billion in online sales. Online retailers might expect Cyber Monday to be the prime promotional day of the year, but I believe this is a mistake. Remember: While Cyber Monday is commonly regarded as an online retailer sales day, almost everyone is online nowadays. Cyber Monday is no longer the online version of Black Friday. Black Friday is.

Black Friday has been growing as an online sale day year after year. In fact, it’s growing faster than Cyber Monday. Even as close as they were in online sales last year, Black Friday grew nearly 22% year over year, whereas Cyber Monday grew only 12%. Expect Black Friday to be the biggest online shopping day of 2017.

If you are planning your peak sales or promotions around these mid-season days, I would make Black Friday the pinnacle. You don’t want to be late to the party and miss out because customers shopped other Black Friday deals. And don’t forget that many retailers will start their Black Friday deals prior to Black Friday. Welcome to Gray November!

Plan for Success

Even the best planning won’t guarantee success. The season is long, and the hill is steep. But we know consumers will shop – and shop early. We know they will browse and buy on mobile devices. And we know every day will be its own little holiday. A bit of internal analysis and time spent planning for these trends will give you the best chance of crossing the holiday finish line with ease.

This was originally published on Multichannel Merchant.

Greg Zakowicz is a eCommerce and retail marketing speaker, analyst, strategist, and award-winning podcaster whose experience spans email, mobile, and social media marketing. More about Greg here.

Alexa, Order Me Browserless Commerce

My five-year-old son recently uttered the phrase, “Why don’t you just ask Siri?” This was in response to my wife asking me a question. Even though my answer, “because I am smarter than Siri” wasn’t fully accepted, something occurred to me. This is his normal.

What does this mean for online retailers and brands that are accustomed to consumers navigating browsers rather than barking voice commands?

My five-year-old son recently uttered the phrase, “Why don’t you just ask Siri?” This was in response to my wife asking me a question. Even though my answer, “because I am smarter than Siri,” wasn’t fully accepted, something occurred to me. This is his normal.

Voice assistants appear to be poised to be the next big thing. After all, outside of emojis, speech is the most natural way to communicate. While assistants like Siri have been adopted for things like answering questions, texting, or setting reminders, the commerce capabilities are emerging. Amazon, Apple, Google, Microsoft, and Alibaba are all in, or getting into, the voice assistant market. While home voice-controlled devices are still new, consumers are showing their willingness to adopt this evolving technology.

What does this mean for online retailers and brands that are accustomed to consumers navigating browsers rather than barking voice commands?

Browserless commerce, or conversational commerce, is still in its infancy. No one really knows what it will look like for sure. I have no doubt that ordering items in bulk, such as diapers and wipes together, will become a reality sooner rather than later. Once that’s tackled, what’s next?

How do Brands and Retailers Fit Into Browserless Commerce?

The first company people think of when it comes to voice ordering is Amazon – and with good reason. But if voice control becomes a major part of people’s daily experience, how will traditional online retailers adapt? Will retailers and brands be forced to sell on Amazon or Jet to have product exposure to customers? Will they be able to create their own browserless commerce “site,” and if so, how will consumers navigate it? Or will more marketplace competitors spring up to compete with Amazon, Jet, and eBay?

There are hurdles. Comparison shoppers and those who use reviews aren’t necessarily going to trust the voice assistant to deliver the right product at the right price. This may be less of an issue for those growing up with these tools. But for today’s shoppers, there needs to be a high level of trust in the device and company.

And how will we browse the internet via voice? Can the voice assistant search reviews and read them to us when we are shopping for a refrigerator? What does this do to advertisements and retargeting strategies?

And more importantly, who controls all of this data, and what will they do with it? If browserless shopping and voice search become an everyday reality, could this lead to the resurgence of offline marketing, like direct mail? Think about it. The data needed by retailers to narrowly target customers will be owned by whatever company is collecting it through their device. Retailers could easily purchase/rent targeted data from these companies (hello revenue stream) for direct-mail or other types of advertising techniques. Theoretically, they would even be able to fine-tune the types of customers they are targeting, from location, lifestyle, and real-time browsing history, just to name a few.

What Does This Mean for Brand Value?

Hey voice assistant, order me glass cleaner. Does it send me Windex or generic glass cleaner? Interestingly, voice-assisted shopping could erode name brands. Voice-ordering glass cleaner from Amazon means you may be automatically shipped a private label brand versus a name brand. Or what if a user uses laundry detergent for sensitive skin, but tires of the price of the brand-name “free and clear” detergent? If they order another detergent for sensitive skin, who makes the decision of which one to send?

As this way of shopping becomes more common, this issue has the potential to expand even further than just these examples. How will retailers react? Will the consumer care, and if so, should they? Remember, older generations might have stronger brand loyalties, but consumers growing up when this is the norm may not. Ordering name brands may be a break from the norm, especially if they are more expensive.

What about searching for other goods, like clothing? How can the browserless experience incorporate visuals? A spoken command could open a synced TV (through a device like a fire stick) or the Echo Show. This would allow consumers to visually browse products initiated by speech. Your voice could control the navigation, allowing you to choose the brand-name product you want. This would allow a site, such as Amazon, to avoid alienating its marketplace sellers, continue to collect ad revenue for higher displayed products, and provide the consumer with a transparent purchase process.

Could Households Be Branded?

Voice assistants are designed to make life “easier.” But connectivity to other electronics in the house is what will truly make life easier. We may be looking at a future where homes are dominated by one brand, like Amazon, Google, or Apple. In this situation, you may have a Google Home device synced with your Nest and Chromecast devices. Intermixing Amazon or Apple products could potentially cause a disruption to your user experience, although a little competitive partnership will almost certainly be required. We may see a day when there are branded homes, with all household devices being synced and owned by one main company.

If there is consolidation around one company’s devices, will these companies go on a spending spree to purchase complementary systems to integrate, like alarm, appliance, or heating and air to provide an all-in-one home solution? I don’t think this will be the case, as fostering integrations seems the likeliest path to consumer adoption, but I wouldn’t be surprised to one day see companies experiment with a one-stop home connectivity approach.

While I may be living through the start of the spoken assistance era, my children will grow up with browserless commerce as the norm. Shopping via voice may seem unnatural for most of us, but it won’t be for them. I look back on pay phones as an example of something that was common when I grew up. Now, if I see one, I am startled at the sight. Ten years from now, my children may look back at smartphones in the same light.

This was originally published on Multichannel Merchant.

Why Your Email Program Sucks

Do your email subscribers find your marketing emails useful? I ran across a statistic from Fluent that suggests consumers think marketing emails are consistently useful only 15% of the time and not useful nearly 60% of the time. So how do you ensure your email program falls into the first category? By ramping up your sophistication.

Do your email subscribers find your marketing emails useful? I ran across a statistic from Fluent that suggests consumers think marketing emails are consistently useful only 15% of the time and not useful nearly 60% of the time. So how do you ensure your email program falls into the first category? By ramping up your sophistication.

I recently presented a session on “Why Your Email Program Sucks.” My goal: Offer my own research on where email marketing is lacking and make the group stop and think about their own brand’s email experience. To provide authentic examples, I signed up for the email programs of five well-known brands, using the same 5-7 email addresses. I wanted to not only assess their effectiveness but how each company used the information I provided (at sign-up, via the preference center, my click, browse, and purchase data) to better target me.

With one email address, I never opened a message. With another, I consistently opened but never clicked. For another, I opened and clicked on the same link in every message. I also used the accounts to manage my preferences, abandon my shopping cart and make purchases. Here are a few questions I wanted to answer:

Did the brand differentiate itself from competitors?

Did they influence me to purchase?

Were the messages timely and relevant?

Did they incorporate my purchase behavior?

The answer was generally a resounding “no.” I only received targeted messages in a few cases. And each time a brand asked for my gender at sign-up, they failed to use it. Post-purchase messaging was lacking in all instances. But this was just the tip of the iceberg. Here are some of my more interesting findings:

Welcome Email Messaging

Three of the five brands asked for my gender at sign-up. None customized the welcome message or series based on that information.

Only one brand sent a traditional welcome series. It was four messages long and contained a social invite and a message inviting me to manage my preferences.

One brand sent me a welcome message every single time I filled out a form and, for some reason, even sent one after I abandoned my shopping cart (two weeks after my original sign-up).

One brand sent two welcome messages. The initial message sent with a from name of “online” was in plain text and included no call to action. A well-designed, branded welcome was sent two days later.

General Messaging and Segmentation

Send cadence to the various email addresses was almost identical, regardless of shopping behavior. Only two brands had slight variations.

Only two of the five brands sent mobile-friendly emails. I was stunned!

No brands included product recommendations in their emails.

Almost all messaging was batch-and-blast.

Only one company sent me gender-based messaging more times than not.

Email open or click activity did not affect the marketing strategy for any of the five brands.

One company signed me up for three sister brands (all related to children) – but it was not for the address that clicked the maternity link in every email.

Abandonment Messaging

Only two brands had a cart recovery strategy. One had only one message, while the other sent two.

None sent browse recovery messaging.

Post-Purchase Emails

No brand included a true post-purchase series.

One brand sent me two product review messages on the SAME day. I should note these came two days after the company issued a return label to me.

Only one brand had optimized its transactional messaging by including sister-brand promos in the message.

One Not-so-fun Fact

One company removed my email address altogether after I updated my preferences. It was also the email from which I opened and clicked on every single message.

I encourage everyone reading this to thoroughly analyze your email program (and other digital marketing tactics) to see how well you’re connecting with your customers. If you see some of the same results, it’s time for a change. Consumers today expect you to listen to them and offer a relevant, personalized experience with your brand. If you don’t deliver, you can kiss those subscribers good-bye.

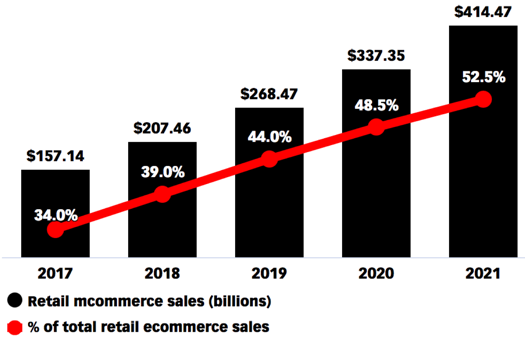

Why 2021 Is Your Mobile Strategy Doomsday

Change with the times, or the times will change you. These words have never been more true than they are today. That’s because mobile devices, especially smartphones, are changing the game for retailers. Mobile is more than just the way emails render. Mobile is the primary way people consume information. Consider this:

Change with the times, or the times will change you.

These words have never been more true than they are today. That’s because mobile devices, especially smartphones, are changing the game for retailers. Mobile is more than just the way emails render. Mobile is the primary way people consume information. Consider this:

eMarketer found that since 2013, mobile devices have gained more than one hour in major media consumption time, up to 3:17, while TV has declined to 4:01.

According to Fluent, the smartphone is the primary device (55%) used to access the internet, while only 26% prefer a laptop or desktop.

What does this all mean for commerce marketers? Has this trend toward mobile been overstated? How quickly are things changing? Let’s take a look at what the industry has been seeing and how you can prepare for what’s coming our way.

The Growth of Online Sales

Year over year, ecommerce is not only growing but taking an increased percentage of total retail sales. According to eMarketer, ecommerce sales accounted for $396 billion last year, which was more than 8% of total retail sales. That’s a significant increase from the year before, with ecommerce sales totaling $343 billions and accounting for 7.3% of total retail sales.

Ecommerce and retail sales 2012-2016

When we look at sales from mobile commerce, 2016 clocked in at nearly $116 billion in sales—29% of total ecommerce sales. In 2015, mobile commerce accounted for nearly $81 billion in sales and 23.6% of total ecommerce sales. Once again, you can see not only strong overall growth, but the increased contribution of mobile to online sales.

Mobile commerce sales 2014-2016

When we hear mobile commerce, we immediately think of smartphones—and rightfully so. They continue to be the go-to mobile device for consumers. In 2016, 58% of mobile sales were made on smartphones, up from 46% the year before. Smartphone purchasing is rapidly increasing year over year. This can’t be ignored.

Smartphone and mobile commerce sales 2014-2016

What’s Next For Mobile Commerce?

It’s time to get serious about mobile. It’s predicted that by 2021, mcommerce will make up more than 50% of total ecommerce sales. While it’s important today to optimize for mobile, not being fully optimized in only a few short years will officially leave you behind the times.

Retail mobile commerce sales 2017-2021

Be prepared. Take time to analyze where you might need improvement. Here are a few things to think about:

Are your checkout pages optimized for mobile? Are they integrated with mobile payment solutions, such as Apple Pay? The days of filling out long forms on mobile devices, manually moving from one box to the next, are on their way out.

Is your website completely mobile-friendly, from search to checkout?

Are your emails designed for mobile?

Are your communications relevant? If emails, recommendations, and search results are not relevant, consumers will simply move on.

According to Statistica, an average mobile user checks their phone 150 times each day. They can do whatever they want, wherever they want, whenever they want. They can find any product they are looking for, regardless of where in the world it’s located. If you don’t provide a frictionless, relevant, up-to-date user experience, someone else will.

Retail Predictions: How Small Retailers Will Change In 20 Years

In the year 2037 we may not quite be on planet Mars, but one thing is certain, the face of retail and ecommerce will have drastically changed, and this is particularly true for smaller retailers and mom and pop shops.

In the third installment of a three-part series, find out how I predict small retailers may change 20 years from now.

FUTURE OF ECOMMERCE: HOW SMALL RETAILERS WILL CHANGE IN 20 YEARS

Mom and Pop stores, once the bread and butter of the retail world, are all but becoming relics of a former time. As large retailers and big box stores sprawled across the country, undercutting prices while offering more inventory, smaller niche retailers simply couldn’t compete. Over the years, many of these shops that would try to plant their seed at a physical location have found that online or ecommerce offerings were more suitable to their needs and means.

From Amazon to Etsy, to Magento Community and Shopify, there are numerous outlets for smaller retailers to get their products in front of consumers. But what happens in 20 years time when these large retailers begin to consume one another, when name brands become less meaningful in place of price and quality, or as the desire for more meaningful experiences becomes vital to product sales? In the year 203,7 we may not quite be on planet Mars, but one thing is certain: the face of retail and ecommerce will have drastically changed, and this is particularly true for smaller retailers and mom and pop shops. I, along with other industry professionals, was asked about how small retailers will change over the next 20 years. Here is what I had to say.

WHAT ROLE WILL PHYSICAL RETAIL STORES PLAY IN CONSUMER BUYING, AND HOW WILL THEY HAVE CHANGED?

Greg: The concept of the store really hasn’t changed in 100 years. Stores have gotten bigger, but in most instances, the fundamentals are the same. You go there to purchase something and take it home the same day. I don’t think this model is doomed, even with advances in technology.

People are social by nature, and I think they will continue to want to touch, experience, and take home purchases on the spur of the moment. Assuming people will always be willing to wait for products is assuming people will no longer want immediate satisfaction. If anything, with the expectation of fast and free shipping, we are moving closer to consumers’ expecting immediate gratification.

It’s possible we will see an increase in store locations, but with less inventory. For this to be successful on a large scale, shipping costs will need to come down. Housing all inventory in several key locations around the country means retailers will have to ship one product at a time, rather than bulk ship to key stores. This might lead to one mega-store in each metropolitan city, with smaller showroom stores around the city. This will allow products to bulk ship locally without forcing retailers to build out distribution hubs around the country. As of today, Amazon and Walmart are probably in the best situation to execute this strategy.

The concept of checkout-less stores is sure to expand over the next 20 years. As technology improves in this space, I think more and more retailers will take to it. I am skeptical that it will be adopted widely by retailers. I think it is better suited to products like clothing than it is for groceries, for example.

WHAT DO YOU BELIEVE TECHNOLOGICALLY OR CULTURALLY WILL BE THE BIGGEST FACTOR IN HOW CONSUMERS BUY IN 20 YEARS?

Greg: Virtual reality and augmented reality will play the biggest role here. I think consumers will be shopping in their living rooms using headsets or other applicable technology, where they can try on products, see holograms, or 3-D views of themselves with products. Similarly, virtual in-store shopping certainly will be more advanced than it is today. People will be able to visually shop their local brick-and-mortar store using VR or AR and have orders shipped to them.

Finally, on this same note, we can expect online-only retailers to create virtual storefronts to better connect consumers with their brands. Where an online retailer used navigation bars to direct people, they can create their own virtual stores that bring together a consistent look and feel for their brand and ease the shopping experience by allowing the user to “walk” through their stores.

WHAT KIND OF JOBS WILL BE NEEDED TO SUPPORT FUTURISTIC RETAIL AND ECOMMERCE BRANDS?

Greg: For virtual stores, we’ll need virtual retail designers or virtual architects. These people will be in charge of designing a virtual floor map, as is done with brick-and-mortar locations. However, knowing what works in the physical retail storefront will be quite different in a virtual storefront. Counter-clockwise shopping, brand merchandising/placement based on eye level, and size of shopping carts are not likely to be as meaningful in an online world. It will be interesting to watch how the online version evolves.

Software engineers are already becoming a permanent fixture for nearly every company, but positions in designing virtual environments, as with video game creators, will become a more common role for retailers or agencies.

I don’t believe the role of a human marketer will go away. Commerce marketing automation will make their jobs easier, surfacing data and related analytics faster, making it easier for marketers to predict ways they can boost revenue. The marketer’s role will continue to shift as consumer adoption of new marketing tactics is accepted and rejected. Humans marketing to humans will always be important.

LASTING THOUGHTS

Greg: I think there will be a time within the next 20 years when there will be a bit of a technology backlash. I think people will crave the “quiet” that comes from being disconnected from the online world. Technology won’t go anywhere, but you may find people sharing less online and doing more in person. This may lead to the re-emergence of brick-and-mortar stores as a destination, much like the shopping malls of years ago.

Click Here to View Other Experts' 20-year Predictions

VIEW MY 5-YEAR PREDICTIONS FOR MID-SIZED RETAILERS HERE

VIEW MY 10-YEAR PREDICTIONS FOR LARGE RETAILERS HERE

Email Expectations vs. Reality: Are You Letting Your Customers Down?

Consumer expectations versus reality. It is a complex topic for all retailers, but especially for those who sell online. Look at how Amazon has raised the bar on consumer expectations, such as with fast and free shipping. Consider how accessible mobile phones are, allowing consumers to find any product they are searching for, regardless of where they or the product is located. Social media, and its integration into the shopping experience, is providing a direct connection between brand and consumer.

Consumer expectations versus reality. It is a complex topic for all retailers, but especially for those who sell online. Look at how Amazon has raised the bar on consumer expectations, such as with fast and free shipping. Consider how accessible mobile phones are, allowing consumers to find any product they are searching for, regardless of where they or the product is located. Social media, and its integration into the shopping experience, is providing a direct connection between brand and consumer.

The best way to meet consumer expectations is to develop a more robust personalization program, especially when it comes to email marketing. According to a 2016 Flagship Research survey, nearly 60% of consumers expect gender to be used to make email messages more relevant. More than 60% of consumers expect emails to be personalized based on interests they gave in their profile, their birthday, purchases they made online, and what they looked at on their website. While these figures are telling, what is even more daunting for retailers is that 40% of consumers expect offline purchases to be used to make email marketing more relevant. I repeat, offline purchases!

The good news is that many of the necessary data points are already being collected by retailers. When it comes to email marketing, retailers often ask for this data at signup or inside of messaging itself. Consumers who provide this information do so willingly, but expect something in return: relevance.

Perception is Reality

Retailers aren’t meeting that expectation. Instead, consumers find marketing emails consistently useful only 15% of the time, and at the same time, consistently find emails not useful nearly 60% of the time. This is a drastic difference between expectations and reality.

The primary reason for this gap is the prevalence of batch-and-blast messaging. Too often, retailers have limited internal resources that prevent them from sending deeply segmented emails to their subscribers. The result is generic messaging aimed at the masses rather than the individual. Whether a subscriber purchased yesterday, last month, or never, they get the same message.

Retailers can upend that habit by honing in on those data points that can make their email marketing more relevant. For instance, retailers can look at the source of the email subscriber. The person signing up from the maternity section of the website is likely much different than the one signing up from the men’s clothing section. The same holds true for those clicking inside emails. The person clicking on maternity links in a message should receive different messaging than the men looking at button-down shirts. After all, they have different needs from your store.

Sixty-two percent of consumers expect their website browsing data to be used to personalize the emails they receive. Give them what they expect by implementing a browse recovery strategy. These messages can be a significant revenue driver for any email program. While these messages are generally clothed as promotional messages (pun intended), they are immediately relevant to the recent online window shopper.

What’s It All Worth?

At the end of the day, does this all really matter? The answer is yes! One retailer did just this and implemented a unique second welcome series message based only on a specific link click in the first message. This targeted message was sent to just 3% of the new subscribers, but generated a 140% lift in total message revenue, compared to the generic second welcome series message. This is the power of relevance!

Only 15% of consumers say that marketing emails are consistently relevant. Your competitors likely know this. Take the initiative to meet consumer expectations before they do.

This was originally published on Multichannel Merchant.

Retail Predictions: How Amazon and Giant Retailers Will Change In 10 Years

In the year 2027, it’s hard to imagine going to the same big box grocery store when already so many technological advancements are making its way into each business. Beyond grocery stores, similar changes can been found in the fashion and general merchandise industries. This poses the question, what will happen to the largest of retailers over the next 10 years? Will there be a shift in physical size? Will experiences become more meaningful than general displays and product availability?

In the second part of a three-part series, find out how I predict giant retailers may change over the next 10 years.

FUTURE OF ECOMMERCE: HOW AMAZON AND GIANT RETAILERS WILL CHANGE IN 10 YEARS

Physical retail stores are closing at a record pace, all while giant brands such as Amazon and Walmart are expanding their digital footprint. Of the largest retailers, they too are shifting to an omnichannel world, though many remain lagging behind. Even grocery stores, the goliaths that commonly take up more physical real estate compared to that of any other retailer, may feel safe for the time being, but disruption is on the horizon. Between grocery deliveries, smaller specialty shops, and online ordering with store pickup, grocery stores of today will function differently in the years to come.

In the year 2027, it’s hard to imagine going to the same big box grocery store when already so many technological advancements are making their way into each business. Beyond grocery stores, similar changes can be found in the fashion and general merchandise industries. This poses the question: What will happen to the largest of retailers over the next 10 years? Will there be a shift in physical size? Will experiences become more meaningful than general displays and product availability? These are the kinds of questions we asked our partners, and here is what they came up with:

FOR GIANTS BRANDS (AMAZON, COSTCO, HOME DEPOT), HOW WILL THEY CHANGE OR ADAPT TO MEET CONSUMER DEMAND IN 10 YEARS?

Greg: From a consumer demand perspective, Amazon is leading and will continue to lead in many of these areas. Their distribution centers and warehouses have put them in a position to provide quick and cheap delivery. However, in 10 years, Amazon may be seen as more than just a retailer, as they are today. Today, they have plenty more to offer, but people think of them as a store. I think they will be seen as more of a media company that sells products. I believe they will continue offering TV-type services, such as network shows, original content, sports programming, and movies.

For big-box retailers, like Home Depot, they will be more aligned to execute on changes in consumer demand. Consumers expect their online and in-store inventory to be accurate and for customer service reps to have a full view of product locations to assist customers. We also expect associates to have a connected device so they can assist as needed. The thing to watch is how they control the user experience after someone leaves the store. Will installers and hired third parties deliver better service than they do now? These hired guns become the face of the organization, and in many cases, they ruin a relationship between the consumer and the brand. The store itself had little to no control over that experience, other than sourcing that third party.

HOW WILL CONSUMERS RECEIVE ITEMS PURCHASED FROM A VIRTUAL OR ONLINE PLATFORM IN 10 YEARS?

Greg: This will depend on areas of the country. In places where there is one mall, and shipping times are longer, I think you’ll see similar footprints as you do now. For larger metropolitan cities, I think the changes will vary a bit by product vertical. As a whole, I believe there will be a shift to smaller store footprints, which will predicate smaller inventories. But this is a double-edged sword because smaller stores are only sustainable with fast and free shipping for the consumer.

I do believe that as consumers become more integrated with technology, their desire for human interaction in-store will grow. This makes the sales associates in these stores more valuable. They become the face of your brand. They become your customer service department. Because they hold more value for the brand, they likely become more of a career position than an hourly worker.

I would not be surprised to see more cohabitation of storefronts, where you have two complementary brands in a single storefront. This can bring the allure of “one-stop shopping” to the offline world, without competing products like you would find in Walmart or Target. It also allows retailers to save on the cost of the physical storefronts while effectively doubling their marketing efforts, as each store would have two marketing departments.

I think the pickup centers will be the most adopted of all of these. These centers may turn into a requirement for free shipping. Shipping is expensive for retailers, especially the last mile, so we could see more free shipping to centers, while having to pay a small fee to have it delivered to your doorstep. Again, this provides consumers a choice of cost versus convenience.

Robots may be employed by select stores to deliver in-store pickups, but retailers should view this as an opportunity to put a human face to the brand. When in-store pickup is managed by a robot, retailers create a very sterile interaction. At that point, what is the emotional connection to the brand?

I am skeptical of drones and don’t believe them to be a long-term delivery solution. There are too many obstacles, such as the potential for lawsuits, terror threats, and general public safety issues, to make this a viable strategy.

LASTING THOUGHTS

Greg: Retail technology is advancing faster than adoption at this point. While exciting times are ahead, 10 years is an eternity for technology. What we see from a shopping perspective in 10 years may be completely alien to us now. I expect browserless commerce (voice control) will have a much larger footprint than it does now. Kids today use Siri and other voice-controlled devices as normal, everyday tools. When they are in their teens and ordering something using their voice, it won’t seem like a new concept. They will already have assimilated the use of that mode of communication.

CLICK HERE TO VIEW OTHER EXPERTS' 10-YEAR PREDICTIONS

VIEW MY 5-YEAR PREDICTIONS FOR MID-SIZED RETAILERS HERE

VIEW MY 20-YEAR PREDICTIONS FOR SMALL RETAILERS HERE

Bridging the Online-Offline Personalization Gap

Consumers are so keyed in about personalization that a recent study found 40% of online shoppers expect that multichannel merchants know about their offline purchases and factor those into their marketing emails. Let me repeat, we’re talking about offline purchases!

Retailers recognize this as a challenge, and are eager to solve it. But realistically, too many retailers struggle to connect their consumer profile data, purchase data, and email data — much less bridge the gap between the online and offline world. Consumers are coming to expect something most retailers are not yet poised to provide.

Consumers are so keyed in about personalization that a recent study found 40% of online shoppers expect that multichannel merchants know about their offline purchases and factor those into their marketing emails. Let me repeat, we’re talking about offline purchases!

Retailers recognize this as a challenge and are eager to solve it. But realistically, too many retailers struggle to connect their consumer profile data, purchase data, and email data — much less bridge the gap between the online and offline world. Consumers are coming to expect something most retailers are not yet poised to provide.

Retailers today need to use the options available to bridge the online-offline personalization gap.

Location-Based Targeting on the Web

Geotargeting is sometimes thought of as exclusively a brick-and-mortar tool – but it shouldn’t be thought of that way. Location-based options exist that can provide a customized and relevant user experience for the online shopper. For example, if a user visits an online clothing retailer’s website in December, the content should be tailored based on their location. Buffalo-dwelling Kyle should have a different online experience than Miami-based Kevin.

What if you only sell warm-weather clothing? User location can help you guide a user not only to a purchase, but also to a higher order total. For example, if Kyle in Buffalo is visiting the site, it may be an indication that he is planning a trip to escape the cold. Your product recommendations may be tailored to upsell complete outfits, or frequently forgotten vacation items, such as sunglasses, waterproof camera cases, or beach bags.

These same principles can apply to marketing emails. Detecting not only an email reader’s location, but also the device they are on, allows you to serve up user-specific content. For example, if they are an avid runner and rain is forecast three days out, you can display content and/or product recommendations showcasing top-rated gear for running in the rain. You might even combine this with an upgraded shipping offer to speed the product to their door – and secure the deal. If they are on a mobile device, you can change the content to be more streamlined, and maybe more interactive, such as offering a video or user-generated content.

The consequences of not doing this can put off customers. Outdoor furniture company RST Brands learned that when it sent out a “Dreaming of Summer” email during the winter and heard back from a Miami customer who pointed out that this is the time of year when people in his area enjoy the outdoors. RST responded with a geotargeting strategy that avoids those kinds of miscues.

Offline Location-Based Targeting

If done right, geotargeting can be a great way to provide a better in-person experience. Let’s say I abandon my shopping cart. Instead of just sending me the general abandoned cart message, I receive a note about the abandoned products and information about a nearby store where I can try on the items I abandoned. That is a great way to create a terrific in-person experience. But retailers need to understand how to provide actual value to nearby consumers to make this work.

Unfortunately, that isn’t always the case. Recently, Yelp announced the acquisition of Wi-Fi marketing company TurnStyle Analytics. At a high level, TurnStyle allows retailers to require a login to access a company’s free Wi-Fi. This allows consumers to opt-in to receiving emails, SMS or social messages from that retailer in exchange for Wi-Fi access. The consumer gets free Wi-Fi and, perhaps, some location-based promotions. The retailer gets to grow their subscriber list. This method offers a lot of benefits for both retailers and consumers, but it also has challenges.

The biggest challenge is that consumers have come to expect free Wi-Fi in public establishments. I know I certainly do! It can be a point of friction for consumers to turn over info just to use Wi-Fi for a brief period. I know if offered the choice, I often opt to use cellular data rather than go through the hassle of inputting my data and deleting messages I don’t want. Consumers have shown they will provide access to their data, but the immediate and long-term value needs to be there.

While this type of geo-targeting can be beneficial, it may lose its long-term effectiveness. Retailers may choose to take the Starbucks method and ensure their Wi-Fi is accessible to everyone, and instead focus on providing excellent customer value through every other stage of customer interaction.

Ultimate adoption and tolerance will be determined by value. If a retailer is not rewarding consumers for providing info, then the ongoing marketing messages, and potentially their entire view of the retailer, may lose their luster.

Connecting the Data

So, while there is value in each example mentioned above, these connection points need to work together to provide a more cohesive consumer experience. Connecting the data is the critical part. Otherwise, your marketing efforts will continue to be fragmented, less valuable, and will leave consumers where they are today…wanting and, more importantly, expecting more.

This was originally published on Multichannel Merchant.

Retail Predictions: How Mid-Size Retailers May Change By 2022

Over the next five years, mid-size retailers such as L.L. Bean, Hasbro, and Wayfair will see large impacts and face the most challenges. While we may not have a crystal ball, industry experts, like Greg Zakowicz, have a direct tap into the changing landscape of retail, so we asked them how they see mid-size retail and ecommerce shifting over the next five years. From emerging technology to shifts in how consumers receive their goods, there are a lot of iterative changes that our industry is likely to see.

In the first of a three-part series, find out how I predict mid-sized retailers may change over the next 5 years.

FUTURE OF ECOMMERCE: HOW MID-SIZE RETAILERS MAY CHANGE BY 2022

Now that emerging technology like virtual reality, beacons, and voice assistants is finding its way into more consumer homes, what role will these play in the future of ecommerce? Not only is hardware improving and creating new ways for consumers to buy goods, but the software, such as artificial intelligence, is improving how products directly correlate with needs and wants.

Over the next five years, mid-size retailers such as L.L. Bean, Hasbro, and Wayfair will see large impacts and face the most challenges. While we may not have a crystal ball, industry experts, like Greg Zakowicz, have a direct tap into the changing landscape of retail, so we asked them how they see mid-size retail and ecommerce shifting over the next five years. From emerging technology to shifts in how consumers receive their goods, there are a lot of iterative changes that our industry is likely to see.

HOW WILL MID-SIZE RETAILERS CHANGE OVER THE NEXT 5 YEARS?

Greg: I don’t expect we’ll see drastic changes from many of them. I think retailers will do more behind the scenes to integrate data sources and share. We might see retailers put more emphasis on improving the overall value they provide to customers by providing more personalization and value-driven loyalty programs, for example. Of course, much of this requires accurate, integrated data. Without that, marketing programs likely will fall short of expectations.

WHICH IF ANY EMERGING TECH WILL BECOME WIDELY ADOPTED WITHIN THE NEXT 5 YEARS?